Stripe Launches L1 Blockchain: Tempo

Here's the play. It's very simple, and it's quite good.

Stripe processes a LOT of money. The customers that get that money need to move it around. Often to banks. Stripe makes no money on that.

Over the last few years, stablecoins have become a preferred means to hold and move money (for convenience, etc).

Stablecoin providers make money on their float -- selling stablecoins means you get free deposits, and risk-free rates are presently around 4%. For every $1M in stablecoins your customers hold, you can make $40k/year. Stablecoin providers like Circle pay about half of that back out to partners that sell the tokens.

Stripe is huge, and well-trusted by customers for handling payments. By adoption stablecoin infrastructure to control financial flows into stablecoins, they can amass huge amounts of stablecoin sales.

If even ~3% of their transaction volume gets held in Stablecoins, and they make 1% a year on that, it's about $1B a year in bottom line.

~$10e9 (daily avg vol) * 365 * 3% (converted to stablecoins) * 1% (net income) = ~$1B

There's a little panel on the bottom right where you can change some parameters of the animation - setting twist high makes some interesting patterns.

I wonder if that's intentional or left in from debugging the animation when it was being created. As-is felt like a nice easter egg and I appreciated it being included.

Ah the layers.

Okay, so one: Obviously pointless from a tech POV. There is nothing that a Stripe controlled blockchain could offer that a database could not.

But then, why? Sadly, as someone who does like the ideals of true cryptocurrency, yet another way to make sure "real" crypto doesn't happen, much like what is happening to BTC.

Here's hoping (yeah, it's a long shot) people see through all of this and maybe, MAYBE, get into the actual ideals of cryptocurrency again.

Didn't a number of companies led by Facebook already attempt to do this with Libra (Diem) and basically got nuked from orbit by US regulators. I have to assume this is primarily happening now because there is a more favorable (nonexistent) regulatory environment.

This is a pretty big deal. Stripe is already processing billions of transactions. Additionally Stripe already has the relationship with merchants that other L1's lack along with the payment network expertise.

If Stripe’s closed-loop system scales, banks and card networks could lose significant transaction volume, fees and even merchant relationships. Merchants and customers win with lower transaction fees. This marks a very credible and large-scale effort yet to challenge the Visa and Mastercard duopoly.

Obviously not perfect and other questionable projects have stained blockchains reputation but it is a net win, no?

[I'm likely missing something, but]

"EVM-compatible, built on Reth" => they're essentially building a private Ethereum fork with a fancy validator selection process.

Couldn't they just get these benefits (predictable fees, fast settlement) by ... running a database between these financial institutions?

If Stripe controls the validator set (even indirectly), then ... just a distributed database with extra steps, no?

This uses blockchain only for marketing buzzwords.

Stablecoins require trusting that the coin issuer doesn't print money. This goes against the core premise of blockchain being trustless!

This is just a payment API with extra steps (all of the integrity and identity features use cryptography that works without blockchain, unless your definition of blockchain is broad enough to include git and matrix chats, then the stripe thing is a blockchain too).

So like 11 years ago, Stripe made investments into Stellar, which was supposed to be a payment network that would facilitate transactions into existing currencies. I think that hasn't really gone where it was hoped?

https://www.irishtimes.com/business/technology/stripe-takes-...

It doesn't look like there's any information about the consensus mechanism, until that's described in detail, it's unclear what the advantages are, or if it really is suited to payments. There are existing algorithms (like Avalanche L1, or some of the Ethereum L2s), which have fast finality particularly suited to the point-of-sale use case.

They cut out a lot of work for themselves expecting stable coins to materialize on their own chain. It's Stripe, so maybe they are allowed to mint their own USD stable coin, but that's one coin. They might have been better off making an L2 on Ethereum. Otherwise they are going to have to run Uniswap in their EVM implementation and hope that liquidity shows up.

I can see Stripe's customers wanting to use a solution that just works and is backed by Stripe's own distributed ledger, but I can't see their customers' customers wanting to do the same. Their customers' customers are going to want liquidity to other tokens, and privacy. At this point I don't think that a payments protocol can succeed unless it provides privacy comparable to Monero, liquidity to a major L1 and its family of tokens, and of course, fast finality.

Unironically excited to learn: Why is this a blockchain? Why could stripe not just do this (maybe better) without the blockchain bit?

I am actually optimistic that, finally, there could be a convincing answer, because stripe does not strike me as the type of company that would do this without a very good reason. (I am slightly less optimistic, because the page itself does not offer an answer to this question, and instead argues for tempo against other blockchains. But only slightly.)

I'm trying to figure out how this is decentralized? "A diverse group of entities" will run validator nodes. This sounds like it's just a Solana clone then.

This would be more exciting if the current steam/itch situation didn't rest (at least partially) on their shoulders as payment processors. Other people in the threads have brought up the lack of regulation and market capture that Stripe enjoys so I won't rehash those points here.

I can't see this as a positive because of how Stripe has behaved in terms of preventing transactions in the past. Although Tempo is behaving more like a b2b model or fintech-specific orgs in this case, the shoe-drop is when they decide a particular bank, or fintech org, or product is not allowed to perform the transaction on their network after the market capture takes place.

Why not use actual Ethereum as a base layer? If you want speed, build (or use) an L2 on top of it.

I can hardly see any value in "yet another private blockchain" — just use a database, duh.

Well I might be creating something for this if the chain is programmable. Its interesting because stripe is a trustable party so far.

> Tempo was started by Stripe and Paradigm, with design input from Anthropic, Coupang, Deutsche Bank, DoorDash, Lead Bank, Mercury, Nubank, OpenAI, Revolut, Shopify, Standard Chartered, Visa, and more.

Does this mean these companies are about to start accepting stablecoins as payment (via Tempo?) some time in the future? Seems out of the ordinary to work with these companies otherwise.

The sales pitch: It's permissionless, but also has baked in compliance. These two things are not compatible. Stripe must comply with US regulation, they aren't going to launch a financial network that is actually permissionless.

> The blockchain designed for payments

So now it’s official? The other blockchains were designed for gambling?

> Tempo is a neutral, permissionless blockchain open for anyone to build on.

> A diverse group of independent entities, including some of Tempo’s design partners, will run validator nodes initially before we transition to a permissionless model.

> Protect your users by keeping important transaction details private while maintaining compliance standards.

Sounds like it actually has potential. This could enable global QR-code payments using and open, decentralized, and private system. Something like fiat cash payments, but digital. I hope that Valve is keeping track of it, for starters.

Looks like they're still using the Trial version of the font (Exposure) on the landing page there... https://www.205.tf/exposure

it will never be full available to us unlike bitcoin or ethereum? this is literally like a fast db? like you people here used to say. Finally HN is right and stripe founders joined on calling fast db a "blockchain" with lie.

they will censor you and block you in blockchain level so literally db for few big companies, lol.

> EVM-compatible, built on Reth

Anyone know what this actually means? Both literally (what is Reth?) and what it means qualitatively: are Stripe’s crypto efforts competing with Ethereum or strengthening it?

Stablecoins are for all practical purposes Numbered Swiss Accounts v2.

I actually don't understand how they were allowed to exist, it's impressive really.

As for reasons, in the US it's probably related somehow to trying to get in good with the current administration.

I wonder if this was initiated by all of the steam and itch.io content getting removed due to payment processor rules. If I remember correctly steam used stripe (at least at one point in time) so it might be trying to get back into that market without being limited by the payment processors above them.

There’s really no need for a separate L1 to do stablecoins. Just build a rollup on Ethereum.

I have nothing intelligent to say about the blockchain aspect, but this is one of the most illegible websites I've encountered recently. What is the purpose of the crazy spaghetti text background and random low-contrast color palette? Why am I given a cosmetic customization panel for what's supposed to be a serious financial product?

They'll censor transactions for things considered icky by your average suit corpo drone won't they?

The job listing[1] for Rust Engineer at Tempo says

> Attributes: High motor

What is meant by that?

[1] https://jobs.ashbyhq.com/tempo-xyz/aab97703-13e2-42e8-9fb9-9...

Does Stripe have the ability to freeze tokens on the blockchain like Tether can?

I question the logic behind trying to introduce a new blockchain in 2025 but I have to acknowledge how fricken cool the scroll animation is here.

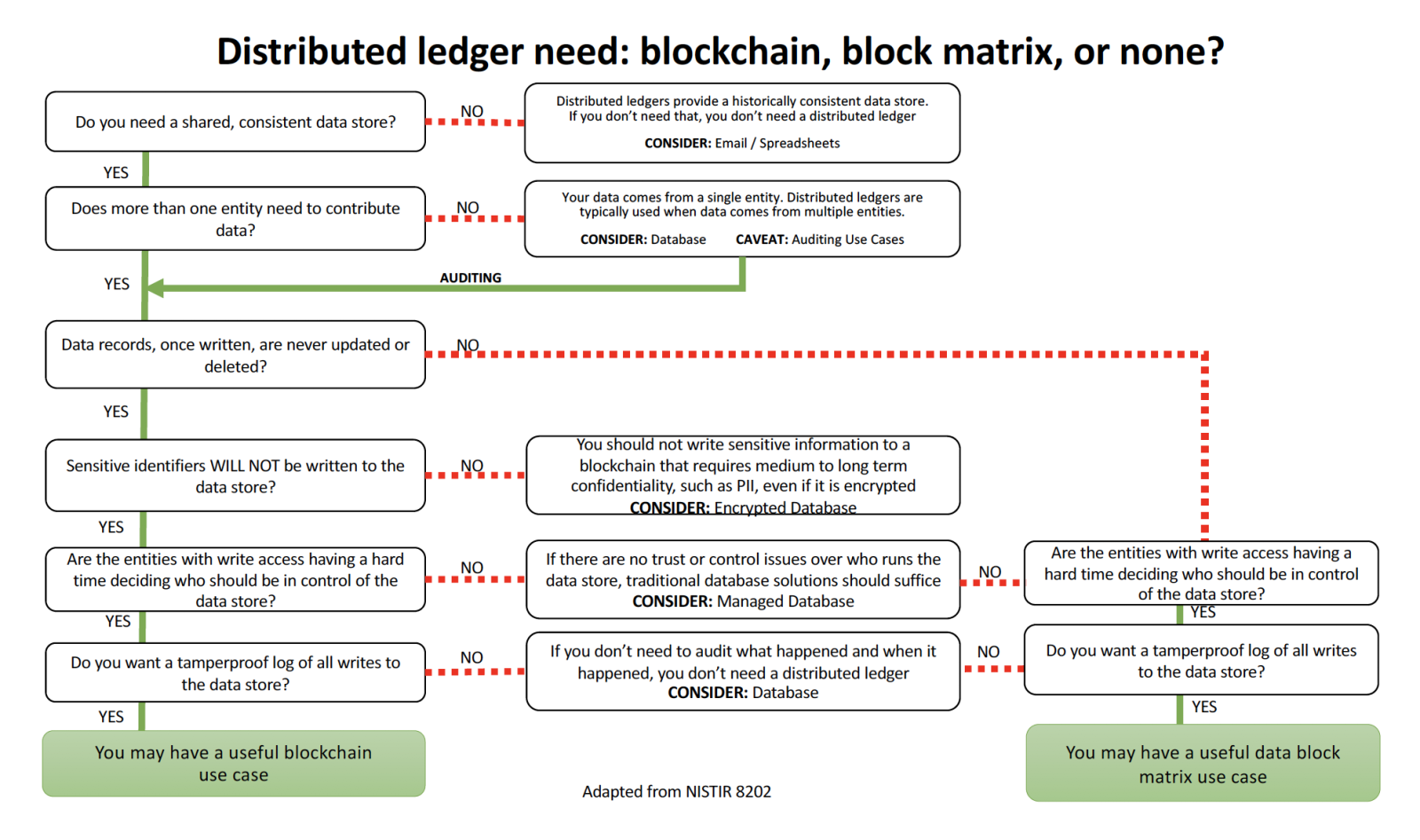

NIST's Blockchain Overview, IR 8202, document often comes top of mind when "blockchain" is mentioned:

* https://www.nist.gov/blockchain

Specifically the yes/no flowchart on whether "you may have a useful blockchain use case" (Figure 6 - DHS Science & Technology Directorate Flowchart):

* https://csrc.nist.gov/CSRC/media/Projects/enhanced-distribut...

{kind=link}

Imagine my delight as a crypto cynic who only admires gold/stablecoin and had recently created a article just for hn (and thus the name) about this... and how stablecoins make sense

But I had literally said that stripe should've actually ventured into and created their own cryptocurrency or something...

Tada, I might be one of the happiest person thinking that I actually really predicted something by my own observations.

here's the blog post: https://justforhn.mataroa.blog/blog/most-crypto-is-doomed-to...

By what I meant most crypto, I meant anything aside from stablecoin (like gold backed/usd backed)

Now that being said, I am still a little critic as to I don't see any offical stripe message and I don't see a way on how it would be implemented?

Like one of the things that I wished in my article was this idea that someone on twitter originally asked where currently if you had money in stripe and wanted to pay it anywhere else, you had to have it enter your bank which might take 14 days and then lets say you want to give it to someone else who has stripe(think anthropic), then they would get it back again after 14 days

So someone basically asked to create something similar to a stripe card. I think that this blockchain is it, except I feel like that you could send money to anyone in a non kyc manner too via this which is again a plus point for sometimes where I feel like that in this world every transaction is usually tracked and as such something like this change is really welcomed.

Once again, can someone really explain what is going to happen in tempo's future as maybe its me who couldn't focus in such a website. I actually went and read the article that the other company that partnered with stripe (paradigm), so I just read paradigm's article: https://www.paradigm.xyz/2025/09/tempo-payments-first-blockc... and they say that it is a new incubator/partnership b/w stripe and them, but would that mean that this tempo is going to be integrated in the stripe ecosystem or no?

I always thought that stripe and stellar had some deep connections but honestly I couldn't care less about it. I don't care about these fake tokens but rather stablecoins/gold stablecoins

Hit spacebar on the website for even more insane visuals!

Re-igniting use cases of blockchain while the current kakistocracy has the regulatory agencies sedated.

Honest question: what kind of problem does this solve?

I think it's more like "SWIFT but using blockchain" instead of Bitcoin competitor. Regardless of that, I wonder how's Bitcoin/ETH's market value with the introduction of Tempo? Since it's like the better version (if you don't mind oligarchy)

What is this supposed to deliver to their users?

product UVP aside, woah! the page is sick!

> A diverse group of independent entities, including some of Tempo’s design partners, will run validator nodes initially before we transition to a permissionless model.

Ah yes, the good old "permissionless" blockchain, that's 100% centralized for just the first 100 years of operation, give or take [subject to updated timelines after 100 years]

I was initially going to reply to someone, but maybe this is useful as its own parent.

In my finance experience, the answer to the "why blockchain" question is settlement. Every banking system (local, international) has a settlement process.

Settlement is where bank counterparties have to tally up who owes whom, and pay each other. That process still takes time internationally, and is complex because of the parties involved.

A more concrete example (I've audited interbank settlements for a local bank in my country):

When I buy something from Amazon as a crossborder transaction with my Visa, my bank and the merchant/bank that Amazon use enter into a counterparty obligation, where in a direct way they'd have to pay each other, incl moving funds between countries. If these 2 banks are the only banks in the world, they can both tally up the transfer of funds to each other, and then pay each other the difference. That'd still take time, right?

Now, we have hundreds of counterparties, using different systems, Visa, MasterCard, Amex, local clearing houses for EFTs, etc. There's also merchants like Stripe who'll be doing the processing, central banks who also ultimately settle currencies among each other. They all have to wait for proof of funds clearing at some level.

If I'm doing an international transfer to my friend, their bank won't want to just credit their account instantly because the time it'll take for them to receive settlement of those funds isn't instant. Else they're going to pay the cost of a deposit that isn't there (let's assume my friend earns interest on positive balances).

The process is that the banks have to recon each clearing house's balance, aggregate that to a list of values like:

* Amex: owes us R200m * Visa: pay them R300m * Clearing house: etc.

Typically the bank's treasury department then effects those transfers. Don't know about other banks, but the bank I audited, it was done by a person daily, their responsibilities are to ensure those settlement aggregates are received/paid, and to resolve differences.

Beneath this person, at that bank, was a team of people who did recons all day. This was in 2012, so hopefully things changed, but I know that team still exists.

Once settlement's taken place, there's another team that verifies international settlements and then approves transfers to my local account. As a data point, it used to take me ~7 days to receive my salary from a US employer while in South Africa.

With crypto, my experience has been that settlement gets delayed, virtualised and distributed because you have a single layer (or still fewer layers across chains).

You send me USDC from wherever, we already don't involve:

* Payment processors like Visa * Central banks as no balance of payments processes are affected * Banks who need to reconcile cross-payments and settle them

Instead, if we're using an exchange (if you're using a local exchange), the funds arrive in the exchange's wallet shortly. The exchange has a constant flow of users buying and selling their local currency. They're in charge of settlement between their wallets and bank accounts.

I'll sell my USDC into my local currency ZAR, and if I withdraw it, the exchange keeps ZAR in local banks, and they send me that money immediately. My crypto salary would be in my bank as ZAR in 30-60 minutes.

Now, I said that crypto delays settlement. My exchange will eventually run out of fiat currency, or need to rebalance. They'll trade some other counterparty exchange, and settle that transaction through SWIFT/equivalent. That settlement will take the 5-7 day process. They just delayed it for their client.

I said it's virtualised because they've skipped the whole process of moving net flows and relied on a central entity, the blockchain, to do that. Ultimately it's a faster process than that backoffice of the bank.

And distributed. Every exchange or remitter has now become their own micro clearing house, and they participate in the banking system by earning their own fees, running their own process.

They only need to interact with each other at higher levels if they need to convert their USDC to US dollars. Interestingly that process happens at one place, but as long as cash and tokens move bidirectionally, the process can get relayed to the point where only a few US banks need to deal with the issuer of USDC.

OMFG STOP TRYING TO MAKE BLOCKCHAIN A THING ALREADY. IT FAILED. MOVE TF ON.

Somebody should start “Killed by Stripe - Stripe Graveyard”[1], because this project soon (several years max) will be featured there.

—-

Why is this better than PYUSD?

How ironic. Why would anyone trust you over bitcoin, which has been around for decades?

Striking while the iron is hot.

You don't need blockchain for that. Total BS.

is this going to be open source?

I know nothing about this technology/service but I do hope it would help avoiding the censorship from Mastercard/Visa.

> A diverse group of independent entities, including some of Tempo’s design partners, will run validator nodes initially before we transition to a permissionless model.

So not decentralized at all. The only reason to not open source validators and allow the public to run their own is to make insiders rich. Another crypto grift that will mint a few millionaires before either being forgotten or merely being used as a speculative instrument.

The whole payment sector is so fucking idiotic. Why would Stripe need a L1? Partnered with paradigm? The company behind every crypto scam in the past 5 years? Who needs this? Who wants this? I just want to order a book from Amazon; why would there be a blockchain?

Who is backing this stablecoin? Who is managing the backing? Where is Tempo located?

Tether has now moved to Bukele's paradise El Salvador and its backing is managed by Howard Lutnick's Cantor Fitzgerald. Previously Tether's funds were managed by Deltec in the Caribbean, a bank with a colorful history.

I guess domains might not mean as much as they used to, but xyz? To me that's something you get for experiments and one-offs, not something you use for a serious enterprise you want to get people onboard for.

I honestly thought this was fake and not from stripe the first time I saw it. (I kinda still do with that domain.)

Unstoppable force: Stripe, an early YC darling, known for really developer friendly payment platform

Immovable object: The perennial HN hate for all things blockchain, complete TLDR energy when it comes to crypto

This should be interesting

why can i do 3-axis orbit control on the animation on the right lmao

I emailed them saying I'm interested, and my message bounced back as spam. ¯\_(ツ)_/¯

I don't get it.

Why does Stripe want to creatively ruin their reputation by venturing into crypto / blockchain?

I don't see anyone in the real world using blockchains at all.

I get AI as it was a real world paradigm shift, but I have never seen anything in this blockchain / crypto space that has reached 100-500 million users let alone 1 billion users, that isn't based on speculation.

The sad irony is that blockchain will do more to promote dictatorship as a superior form of government around the world than any other technology.

Blockchain's primary usefulness has been to evade regulations, and due to the rapidly changing nature of the technology, representative democracies with legitimate legal institutions have lagged behind when it comes to regulating it.

The country that wins (prevents fraudsters and scammers who exploit crypto) will be a dictatorship solely because a dictatorship is the only form of government fast enough to either rein in lawless cryptofinance, or exploit it maximally.

When enough actual value creating people who bought in to the libertarian crypto fantasy finally realize that they're slaving away to make ends meet in an economy that enshrines meme coin shills and folks who use crypto to evade the law, it will have been too late.

The folks on Hacker News seem pretty anti-crypto, but I feel like they're missing the point. If we're actually looking for ways to fix the US debt, stablecoins are definitely worth considering

Not to be confused with Toronto Tempo https://torontotempo.com

This is off-topic to their grand blockchain adventures, but I need to mention it:

I would love for stripe to start paying appropriate VAT on transactions between their merchants and EU citizens, I've been on their ass about it for nearly a year now. I've reported multiple merchants to them which simply refused to provide an VAT invoice for any transactions. Legally, merchants outside EU are required to pay VAT on their B2C transactions if their EU transaction volume goes above a certain limit, and provide VAT invoice for B2B transactions (but with 0% VAT because it is B2B).

But unfortunately Stripe doesn't seem to have the technology to do a SUM(*) in their database, or check if an email address ends in '.de' or '.it' when they take the payment. So they simply do not give a damn if their merchants provide an invoice with the transaction or not.

Oftentimes it was the problem to actually get an invoice document which has company name, company registration number, street address, city, and tax ID. Extremely basic information which is required on all EU invoices. Many times I have submitted invoices from Stripe merchants to my tax accountant and my tax accountant told me that those are not proper invoices and to please reach out to the merchant to get EU-legal invoices.

Stripe has the technological capabilities to implement proper compliance checks, but they choose to let their merchants send you rubbish self-made PDF invoices with a big red "paid" stamp without any information or "official" Stripe invoices with total fantasy names and fantasy company information. You never know if your merchant is sitting in an embargoed country or is just some schmuck from San Francisco trying to hide their ties to a website.

If other HN users from the EU have been fighting Stripe to get EU-compliant VAT invoices for their B2B or B2C purchases, please feel free to reach out. I've been doing a big stink about this and to me it feels like a deliberate pattern of enabling their merchants to ignore EU VAT obligations.

It's really sad that my extremely positive impression of Stripe has been deeply tainted by this kind of experience across various purchases and subscriptions with Stripe merchants. I had to spend so much time pleading with them to provide proper invoices.

[flagged]

Welcome to crypto project number 206701341. At least that is how many are listed on CoinMarketCap:

https://coinmarketcap.com/charts/number-of-cryptocurrencies-...

Bitcoin is decentralized because the sun distributes energy somewhat evenly across the globe.

The other 206701340 crypto projects, including this one, are decentralized because ... ?

From the very sparse info on the page, it seems this project does what so many other chains do to make payments faster and cheaper: They log them on a database that is synchronized across only a few computers.

In other words: I can't find any info on that page explaining how they plan to achieve decentralization.

Blockchain is such a useful and needed technology for mass adoption, yet so redundant to have in the US because of how much side-eye treatment it gets. Blockchain makes more sense to have here than anywhere else in the world. blockchain does not need to handle high transaction rate the same as visa or MasterCard protocols. There needs to be micro workers that can handle transactions in real-time in Blockchain methodology should be reserved for when recording these transactions. The whole point to have Blockchain is to maintain integrity and security, there is no need for this technology to do small tasks when something else can do that more efficient and successfully, When making this technology efficient, you tend to lose the essence of what that technology is representing in the first place IMO.

There are lots of crypto skeptics on HN (and we ourselves were disappointed with crypto's payments utility for much of the past decade), so it might be interesting to share what changed our mind over the past couple of years: we started to notice a lot of real-world businesses finding utility in stablecoins. For example, Bridge (a stablecoin orchestration platform that Stripe acquired) is used by SpaceX for managing money in long-tail markets. Another big customer, DolarApp, is providing banking services to customers in Latin America. We're currently adding stablecoin functionality to the Stripe dashboard, and the first user is an Argentinian bike importer that finds transacting with their suppliers to be challenging.

Importantly, none of these businesses are using crypto because it's crypto or for any speculative benefit. They're performing real-world financial activity, and they've found that crypto (via stablecoins) is easier/faster/better than the status quo ante.